XRP Cross-Border Payments: IMF Recognition Signals Infrastructure Shift

The International Monetary Fund’s recognition of XRP as one of three viable models for next-generation payment infrastructure marks a turning point in the asset’s legitimacy, but the real story is what’s happened since. A March 2023 IMF Fintech Note authored by Financial Counsellor Tobias Adrian explicitly named Ripple’s XRP alongside Stellar and Strike as solutions that have made “substantial progress” addressing cross-border payment inefficiencies. Combined with the SEC lawsuit resolution and accelerating institutional adoption, XRP is transitioning from speculative asset to genuine infrastructure play. The question is no longer whether blockchain can disrupt the $200+ trillion cross-border payments market, but which solutions will capture meaningful share.

What the IMF Said About XRP Cross-Border Payments

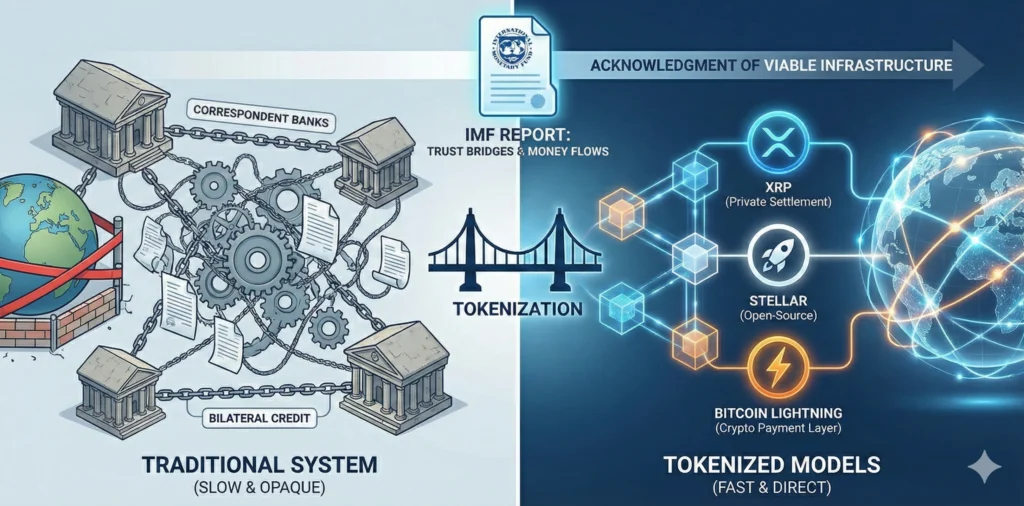

The IMF’s “Trust Bridges and Money Flows” report tackles a foundational problem: cross-border payments remain “expensive, slow, and opaque” because they depend on complex trust relationships between correspondent banks. Moving money internationally requires chains of bilateral credit agreements, each adding cost and friction. The fixed costs of building these trust links have created what the IMF calls “an expensive and concentrated system.”

The report proposes that tokenization could fundamentally alter this dynamic by enabling direct ownership transfers on shared ledgers. Within this framework, the IMF identifies three models already operating: Ripple’s XRP as a private settlement asset and marketplace, Stellar’s open-source protocol, and Strike leveraging Bitcoin’s Lightning Network. The document states that assets like XRP “could integrate into a larger marketplace for global digital payments.”

Crucially, this represents acknowledgment rather than endorsement. The IMF presents XRP as one viable approach among several. But the significance lies in senior IMF officials treating XRP as a serious infrastructure solution rather than merely another cryptocurrency. The January 2025 response from the Institute of International Finance representing 450+ financial institutions reinforced this positioning, formally acknowledging that “Ripple’s network provides an alternative infrastructure for cross-border payments using XRP” in a consultation with the Bank for International Settlements.

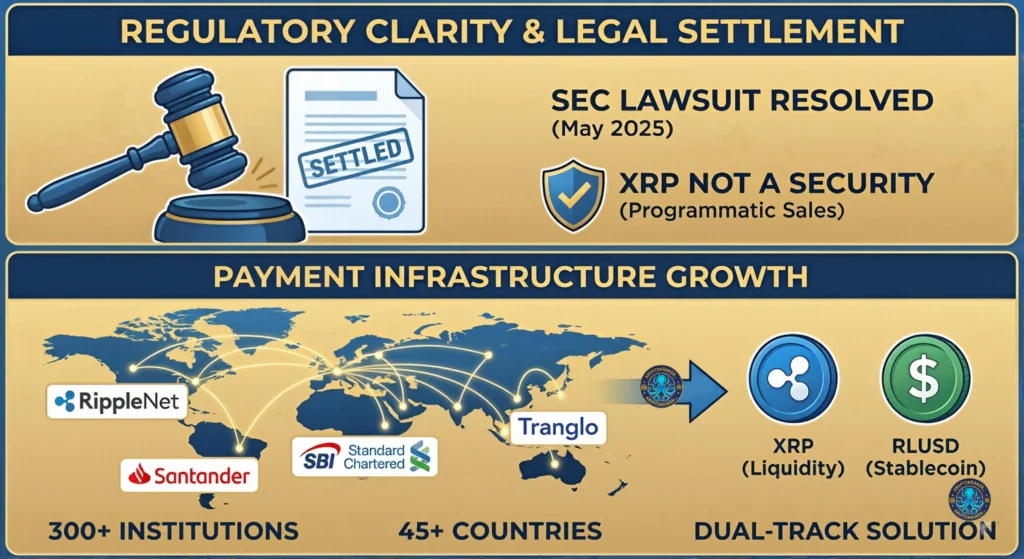

Regulatory Clarity Unlocks XRP Payment Infrastructure Growth

The SEC lawsuit’s resolution has removed the regulatory overhang that constrained U.S. institutional adoption. Judge Analisa Torres’ July 2023 ruling established that XRP sold programmatically on exchanges does not constitute a security, a landmark distinction that survived the appeals process. The final May 2025 settlement saw Ripple pay $50 million to the SEC (down from the $2 billion initially sought), with all appeals dismissed by August 2025. XRP’s legal status in U.S. secondary markets is now settled law.

This clarity has coincided with substantial network expansion. RippleNet now connects over 300 financial institutions across 45+ countries, with coverage spanning 90% of daily foreign exchange markets. Key partners include Santander, SBI Holdings, Standard Chartered, and Tranglo, which operates 25+ payment corridors across Asia-Pacific after Ripple acquired a 40% stake. The company secured a Dubai Financial Services Authority license in March 2025, becoming the first blockchain-enabled payments provider licensed in the DIFC. Japan remains dominant with 61+ banks joining the RippleNet consortium, accounting for more than half of global On-Demand Liquidity volume.

The December 2024 launch of RLUSD, Ripple’s dollar-backed stablecoin approved by the New York Department of Financial Services, addresses a persistent institutional objection: XRP’s price volatility. RLUSD offers enterprises the blockchain settlement benefits without currency risk, with its market cap exceeding $1 billion by November 2025. Ripple has integrated RLUSD into its cross-border payment solution, creating a dual-track approach: XRP for liquidity-seeking corridors, RLUSD for volatility-sensitive enterprises.

XRP vs SWIFT: The Cross-Border Payments Competition Heats Up

XRP’s primary competition isn’t other cryptocurrencies. It’s SWIFT’s modernization efforts and emerging CBDC frameworks. SWIFT gpi, launched in 2017, now processes $300 billion daily with 60% of payments reaching beneficiary banks within 30 minutes. The November 2025 deadline for ISO 20022 migration has standardized data formats across the network, enabling better straight-through processing. SWIFT hasn’t stood still while blockchain matured.

JPMorgan’s Kinexys platform (formerly Onyx) has processed over $1.5 trillion since 2020, averaging $2 billion daily in blockchain-based institutional transfers. Unlike XRP’s open network, Kinexys operates as a permissioned system limited to JPMorgan clients, but that client base includes Siemens, BlackRock, and FedEx. The bank is adding on-chain foreign exchange capabilities in 2025.

The CBDC question looms largest. Project mBridge, involving central banks from China, the UAE, Thailand, Hong Kong, and Saudi Arabia, reached minimum viable product status in mid-2024, processing $22 million in pilot transactions. This multi-CBDC platform could enable real-time cross-border settlement between participating nations without touching Western financial infrastructure. Project Agorá, backed by the BIS and seven major central banks including the New York Fed, is testing tokenized deposits alongside wholesale central bank money. Ripple has secured CBDC partnerships with ten governments including Bhutan, Palau, and Georgia, positioning itself as infrastructure provider rather than competitor to sovereign digital currencies.

Why the Cross-Border Payments Market Needs XRP

The fundamental economics favor blockchain solutions. Global average remittance costs remain 6.2%, more than double the G20’s 3% target for 2027. Sub-Saharan Africa faces fees approaching 8%. Traditional correspondent banking requires financial institutions to maintain pre-funded nostro accounts across corridors, tying up capital. A single wire transfer can touch five or six intermediary banks, each extracting fees.

XRP’s On-Demand Liquidity addresses this directly: rather than pre-positioning funds globally, institutions can convert local currency to XRP, transfer across the ledger in 3-5 seconds, and convert to destination currency on arrival. Ripple claims ODL eliminates the need for pre-funded accounts entirely, representing dramatic capital efficiency gains. The $70 billion in cumulative payment volume processed through RippleNet demonstrates this isn’t theoretical, though it’s worth noting that many RippleNet partners use the messaging layer without utilizing XRP itself.

The ISO 20022 migration creates unexpected synergy. Both SWIFT and major blockchain protocols now speak the same standardized data language, meaning tokenized solutions can interface more cleanly with existing banking infrastructure. SWIFT has tested connections with Ripple, Stellar, and other networks, acknowledging that blockchains are being built using ISO 20022’s data dictionary. Integration, not replacement, may be the near-term path.

What Determines the Future of XRP Cross-Border Payments

Three developments will determine whether XRP captures meaningful market share. First, ETF approval: eleven XRP ETF products appeared on the DTCC list following Ripple’s Swell conference in November 2025, with Franklin Templeton and Grayscale products launching on NYSE Arca. Spot ETF approval, expected by analysts in mid-2026, would open institutional allocation channels beyond direct custody.

Second, the RLUSD strategy must prove out. Enterprise adoption of XRP itself has been limited by volatility concerns and compliance friction. RLUSD offers a dollar-stable entry point to Ripple’s payment rails, potentially expanding the addressable market beyond companies willing to hold XRP directly. The stablecoin’s integration with Ripple Payments in April 2025 and subsequent expansion into Africa via Chipper Cash and VALR signals this is becoming core strategy rather than ancillary product.

Third, CBDC interoperability will matter enormously. If central bank digital currencies dominate cross-border settlement, as mBridge and Agorá suggest they might, XRP’s value proposition shifts from replacement to bridge currency between sovereign systems. Ripple’s government partnerships position it for this role, but execution remains uncertain.

For retail investors considering XRP exposure ahead of potential ETF approval, securing your assets properly should be a priority. Hardware wallets like the Ledger Nano X keep your private keys offline and protected from exchange hacks or platform failures. If you’re new to hardware wallets, our guide on setting up a Ledger device walks you through the process step by step.

The Outlook for XRP in Global Payments

The IMF report, IIF acknowledgment, and Volante recognition collectively establish something the crypto industry has long sought: serious institutional consideration of blockchain rails for mainstream finance. XRP isn’t the only solution these institutions recognize. Stellar, JPM Coin, and CBDC frameworks all received similar treatment. But XRP has achieved regulatory clarity in its largest market, built meaningful network effects across 45+ countries, and launched a compliant stablecoin to address volatility concerns.

The cross-border payments market’s inefficiencies are real, measurable, and affect billions of people and trillions in capital. Whether XRP captures the 14% of SWIFT’s volume that CEO Brad Garlinghouse projects by 2030 remains highly uncertain. What’s no longer uncertain is that tokenized settlement infrastructure, including XRP, has earned a seat at the table where these decisions will be made.

For more on why XRP could reshape global finance, check out our deep dive into fair market value analysis and the BRICS coalition’s interest in Ripple technology.

Disclaimer: This article is for informational purposes only and does not constitute financial, investment, or legal advice. Cryptocurrency investments carry significant risk, and you should conduct your own research and consult with a qualified financial advisor before making any investment decisions. The author and KryptoKraken are not responsible for any losses incurred based on the information presented here.

Disclosure: This article may contain affiliate links. If you purchase a product through our links, such as the Ledger Nano X, we may earn a commission at no additional cost to you. We only recommend products we believe provide value to our readers.